Whether it’s tariffs, trade wars, or post-pandemic inflation caused by kink-ridden supply chains and what many experts believe to be excess money printing, inflation is an insidious drag on businesses’ operations. When it comes to energy’s contribution to inflation, the U.S. Energy Information Administration (EIA) reports that crude and natural gas prices in 2022 have increased on an annualized and weekly basis. Looking at the snapshot of 7/21/2022, WTI crude on the futures market was $96.35 a barrel. This was up more than $26 compared to 12 months ago, and $0.57 higher than a week earlier. For the same time frame, natural gas futures were $7.932/MMBtu, an increase of $3.973 from 12 months ago and an increase of $1.332 from a week earlier.

Whether it’s tariffs, trade wars, or post-pandemic inflation caused by kink-ridden supply chains and what many experts believe to be excess money printing, inflation is an insidious drag on businesses’ operations. When it comes to energy’s contribution to inflation, the U.S. Energy Information Administration (EIA) reports that crude and natural gas prices in 2022 have increased on an annualized and weekly basis. Looking at the snapshot of 7/21/2022, WTI crude on the futures market was $96.35 a barrel. This was up more than $26 compared to 12 months ago, and $0.57 higher than a week earlier. For the same time frame, natural gas futures were $7.932/MMBtu, an increase of $3.973 from 12 months ago and an increase of $1.332 from a week earlier.

When it comes to businesses using any type of commodity, they’re faced with the question of how to raise retail prices when their prices increase. However, many business owners are hesitant to increase prices on their goods and services as they fear it will drive away customers. But in light of increasing input prices, not implementing price increases correctly will impact a business’s earnings and profitability.

As McKinsey & Company explains, there are many considerations why businesses have had trouble with mitigating costs in light of rising input costs. It’s important to monitor raw material costs with a fine-tooth comb. Businesses that bury costs of commodities, labor or tariffs under general accounting categories hide spikes in input costs due to factoring ancillary costs. If volatile input or uncontrollable factors, however, like tariffs can be monitored independently and in real time, businesses are more likely to be able to increase prices – and do so more gradually. With this in mind, McKinsey & Company highlighted four practices that businesses can implement to combat pressure from input costs and pushback from customers who question the reason for price increases.

1. Create a Database of Dynamic Costs

By looking at historical records going back as far as 36 months, businesses can determine trends and keep track of increases or decreases of input materials to share with the sales and customer service department, who can then communicate with customers. Along with looking at how contracts are written and if there are escalator clauses that permit conditions to adjust for increases in input materials, taking steps to accurately measure the impact of raw material costs can be helpful for price increase considerations.

It could look at costs by department. If a plating department at a manufacturing company plates 50,000 pieces of metal a month, incurs $200,000 of direct material costs and has $50,000 in labor and overhead costs, it can be broken down into a per unit cost of $4 for materials and $1 of labor and overhead costs. If the per unit cost of materials fluctuates, investigation can occur through the supply chain from the supplier to the price of futures contracts to see if prices can be negotiated or must be increased for customers.

2. Mind the Economy

Businesses are advised to keep an eye on current economic conditions. This is how companies can set a dynamic pricing strategy. Building on the first step, it’s advised to index prices to those of commodities to reduce the lag time between when companies experience changes in costs for their input materials and when retail prices actually reflect the true cost to the company. Be it fuel, wood, coffee or metals, understanding how the price of commodities fluctuates in real time is essential to determine when and how to adjust prices for retail customers. It also can help businesses determine how competitors are adjusting their pricing to customers, how far prices could increase, and how to augment delivery of goods or services to stay competitive and profitable.

In addition to escalation clauses, companies adapting to changing input material prices could, for example, introduce shorter-term contracts, look for more competitive suppliers, or substitute different but equal quality/performance materials.

3. Coaching Staff to Educate and Explain Price Fluctuations

Continual evaluations for sales teams are imperative. Supervisors must see what accounts have (and have not) been informed of price increases. They should focus on what accounts have accepted price increases (and what level of price increases have been accepted). They also should look at what accounts are likely to accept price increases and what accounts are not likely to accept price increases. Businesses also must factor in the business cycle for the sales process and how each account is performing relative to its price increase targets due to cyclical increases in input commodity prices and interest rates for financing availability. Ongoing coaching should be implemented to identify major issues and ways to resolve them. Anticipating and preparing sales representatives for customer questions through role playing can help better prepare employees to explain why price increases are a part of doing business.

4. Managing Performance

Businesses must play the long game after products or services have been priced accordingly to commodity and input prices. Since inflation follows the economic cycle, upside and downside pricing dynamics can catch companies off guard. Consistently updated product or service pricing systems and prepared sales teams can lead to more profitable margins and hopefully the ability to weather volatile and long-term price spikes.

Much like the price of commodities and labor fluctuate based on dynamic market conditions, finding ways to adapt one’s business practices can increase chances of surviving and thriving in a challenging economy.

Sources

https://www.bls.gov/news.release/ppi.nr0.htm

https://www.eia.gov/

https://www.mckinsey.com/business-functions/growth-marketing-and-sales/our-insights/defying-cost-volatility-a-strategic-pricing-response

Supreme Court Police Parity Act of 2022 (S 4160) – In response to potential threats and protests outside the homes of Supreme Court judges following a leak of their preliminary judgement on a case related to Roe vs. Wade, this bill authorizes extra security for the justices and their families. Specifically, Supreme Court justices and their families would be provided with security detail similar to that of other top government officials and families in the executive branch (e.g., the president and vice president) and legislative branch (e.g., Speaker of the House and Senate Majority Leader). This type of detail generally cannot be declined. The bill was introduced by Sen. John Cornyn (R-TX) on May 5. It passed in both the Senate and the House on June 14 and was signed into law by the president on June 16.

Supreme Court Police Parity Act of 2022 (S 4160) – In response to potential threats and protests outside the homes of Supreme Court judges following a leak of their preliminary judgement on a case related to Roe vs. Wade, this bill authorizes extra security for the justices and their families. Specifically, Supreme Court justices and their families would be provided with security detail similar to that of other top government officials and families in the executive branch (e.g., the president and vice president) and legislative branch (e.g., Speaker of the House and Senate Majority Leader). This type of detail generally cannot be declined. The bill was introduced by Sen. John Cornyn (R-TX) on May 5. It passed in both the Senate and the House on June 14 and was signed into law by the president on June 16. Today, businesses have to grapple with vast amounts of data from different sources, including emails, mailing lists, customer orders, system logs, mobile apps, social media networks, etc. This data is crucial to businesses in various ways. When analyzed, a business can identify operational issues, personalize the customer experience and manage supply chains – all contributing to better decision-making.

Today, businesses have to grapple with vast amounts of data from different sources, including emails, mailing lists, customer orders, system logs, mobile apps, social media networks, etc. This data is crucial to businesses in various ways. When analyzed, a business can identify operational issues, personalize the customer experience and manage supply chains – all contributing to better decision-making. We’re all feeling the pain at the pump. Unless you decide to walk, bike or take public transportation, you might feel stuck. But all is not lost. Here are some fuel-efficient driving techniques that can help you save hundreds of dollars in fuel each year.

We’re all feeling the pain at the pump. Unless you decide to walk, bike or take public transportation, you might feel stuck. But all is not lost. Here are some fuel-efficient driving techniques that can help you save hundreds of dollars in fuel each year. Corporate profits, according to the Bureau of Economic Analysis, grew by $20.4 billion in the final quarter of 2021, a 0.7 percent increase. For the first quarter of 2022, corporate profits fell by 2.3 percent or $66.4 billion. On an annualized basis, corporate profits fell 5.2 percent in 2022, but grew 25 percent in 2021. With the economy facing inflation, the uncertainty of the Russia/Ukraine conflict, and the world working its way out of the COVID-19 pandemic, economic uncertainty abounds. For companies, measuring margins is one way to evaluate performance and strategize ways to survive and thrive in a dynamic economy. Here are a few common margins that businesses can determine to measure their financial performance.

Corporate profits, according to the Bureau of Economic Analysis, grew by $20.4 billion in the final quarter of 2021, a 0.7 percent increase. For the first quarter of 2022, corporate profits fell by 2.3 percent or $66.4 billion. On an annualized basis, corporate profits fell 5.2 percent in 2022, but grew 25 percent in 2021. With the economy facing inflation, the uncertainty of the Russia/Ukraine conflict, and the world working its way out of the COVID-19 pandemic, economic uncertainty abounds. For companies, measuring margins is one way to evaluate performance and strategize ways to survive and thrive in a dynamic economy. Here are a few common margins that businesses can determine to measure their financial performance. One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

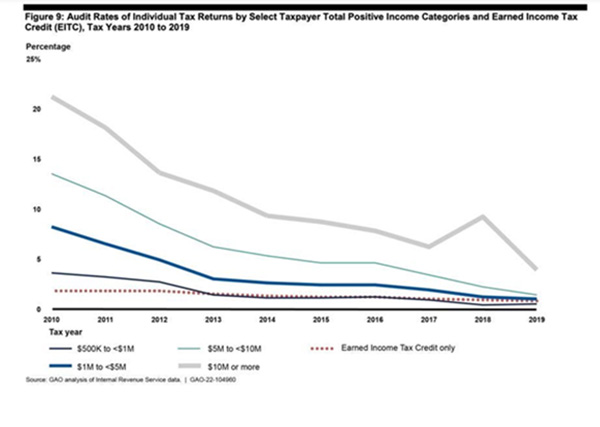

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

To amend the Child Nutrition Act of 1966 to establish waiver authority to address certain emergencies, disasters and supply chain disruptions, and for other purposes. (HR 7791) – In response to the recent nationwide shortage of infant formula, Congress passed a bill authorizing $28 million to fund emergency supplies and to address the potential for future shortages due to emergencies, disasters or supply chain disruptions. The bill was introduced by Rep. Jahana Hayes (D-CT) on May 17. It passed in the House on May 18 and unanimously in the Senate on May 19. It is currently awaiting signature by the president.

To amend the Child Nutrition Act of 1966 to establish waiver authority to address certain emergencies, disasters and supply chain disruptions, and for other purposes. (HR 7791) – In response to the recent nationwide shortage of infant formula, Congress passed a bill authorizing $28 million to fund emergency supplies and to address the potential for future shortages due to emergencies, disasters or supply chain disruptions. The bill was introduced by Rep. Jahana Hayes (D-CT) on May 17. It passed in the House on May 18 and unanimously in the Senate on May 19. It is currently awaiting signature by the president. Cash flow awareness is vital in running the day-to-day activities of a business. Keeping track of the inflows and outflows helps a company make better plans and decisions, such as the right time to expand. Cash flow knowledge reveals where a business is spending money and can protect business relations, among other benefits. However, tracking cash flow is a challenge for many businesses.

Cash flow awareness is vital in running the day-to-day activities of a business. Keeping track of the inflows and outflows helps a company make better plans and decisions, such as the right time to expand. Cash flow knowledge reveals where a business is spending money and can protect business relations, among other benefits. However, tracking cash flow is a challenge for many businesses. You love summer, don’t you? School’s out, and BBQs are on. But what you probably don’t love are those higher air conditioning bills. Here are some tried-and-true ways to help lower the cost of keeping cool.

You love summer, don’t you? School’s out, and BBQs are on. But what you probably don’t love are those higher air conditioning bills. Here are some tried-and-true ways to help lower the cost of keeping cool. The Cash Conversion Cycle, also known as the Net Operating Cycle, answers the question, “How many days does it take a company to pay for and generate cash from the sales of its inventory?” However, before an analysis like this can take place, it’s important to consider the company’s primary line of business.

The Cash Conversion Cycle, also known as the Net Operating Cycle, answers the question, “How many days does it take a company to pay for and generate cash from the sales of its inventory?” However, before an analysis like this can take place, it’s important to consider the company’s primary line of business.